Navigating Tax-Advantage Retirement: Roth IRAs and Roth 401(k)s Explained

In the realm of retirement planning, two tax-advantaged options stand out for their simplicity and powerful benefits: Roth IRAs and Roth 401(k)s. Whether you're just starting your financial journey or nearing retirement, understanding these options is essential for building an independent financial future. Let's explore what Roth IRAs and Roth 401(k)s are, why they're important, and the key advantages they offer, along with a glance at income and contribution limits.

What are Roth IRAs and Roth 401(k)s?

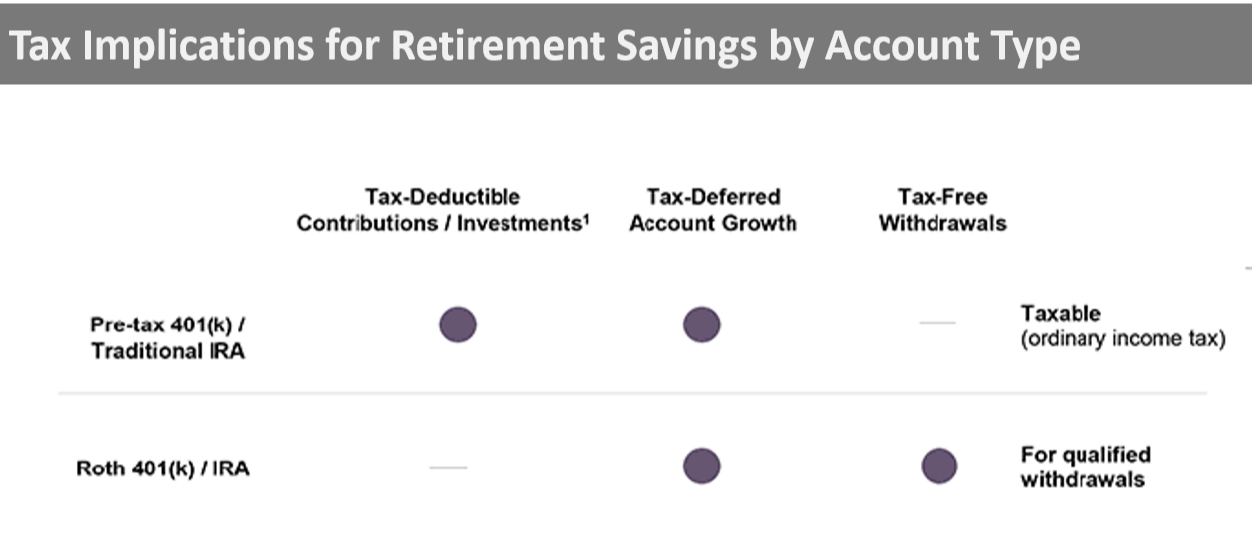

Roth IRAs: A Roth IRA is a type of individual retirement account that allows you to contribute after-tax dollars. The contributions grow tax-free, and qualified withdrawals, including earnings, are tax-free in retirement. Roth IRAs offer flexibility, allowing you to access contributions (but not earnings) penalty-free at any time.

Roth 401(k)s: A Roth 401(k) is a retirement savings plan offered by employers that combines features of traditional 401(k)s with Roth IRA tax advantages. Contributions are made with after-tax dollars, and like Roth IRAs, earnings grow tax-free. Unlike Roth IRAs, Roth 401(k)s have higher contribution limits and may be subject to Required Minimum Distributions (RMDs) during the account holder's lifetime if not rolled over to a Roth IRA.

Why Are Roth Options Important?

Roth IRAs and Roth 401(k)s play a crucial role in retirement planning for several reasons:

- Tax-Free Growth: Both Roth options offer tax-free growth on investments, allowing your savings to compound more rapidly over time without the drag of taxes.

- Tax-Free Withdrawals: Qualified withdrawals from Roth accounts in retirement are entirely tax-free, providing a valuable source of tax-free income during retirement.

- Flexibility: Roth accounts offer flexibility in withdrawals, allowing you to access contributions penalty-free at any time for various financial goals, such as purchasing a home or covering unexpected expenses.

Advantages of Roth Options:

- No RMDs (Roth IRAs Only): Roth IRAs are not subject to RMDs during the account holder's lifetime, offering greater flexibility in retirement planning and allowing for continued tax-free growth.

- Higher Contribution Limits: Roth 401(k)s have higher contribution limits compared to Roth IRAs, allowing you to contribute more towards your retirement savings each year.

Income and Contribution Limits for 2024:

As of 2024, Roth options have income and contribution limits to consider:

- Income Limits: For Roth IRAs, phase-out begins at a Modified Adjusted Gross Income (MAGI) of $140,000 for single filers and $208,000 for married couples filing jointly. Roth 401(k)s have no income limits.

- Contribution Limits: The maximum contribution to a Roth IRA is $7,000 for individuals under 50 years old and $8,000 for those aged 50 and over, including catch-up contributions. Roth 401(k) contribution limits vary by employer and plan, but they are generally higher than Roth IRA limits.

Conclusion:

In summary, Roth options offer straightforward yet powerful solutions for tax-free retirement savings. Whether you choose a Roth IRA or a Roth 401(k), taking advantage of these tax-advantaged accounts can significantly enhance your retirement readiness. By understanding the benefits, contribution limits, and potential considerations like RMDs, you can make informed decisions to secure a financially comfortable retirement.

Source: Roth IRAs | Internal Revenue Service (irs.gov)

The opinions voiced in this material are for general information only and are not intended to provide specific advice or recommendations for any individual.

This information is not intended to be a substitute for specific individualized tax or legal advice. We suggest that you discuss your specific situation with a qualified tax or legal advisor.

No strategy assures success or protects against loss.